|

|

TRANSFORMATION OF INDIA

The population of India is going to reach 1.5 bn people in the next few years:

- We will be the largest market in the world for the next 100 years.

- About 1 bn will be below the age of 35 with an average age of 28 years. Hence for the next 50 years, we will be having the world's largest working population.

- Hence in the next 5 to 10 years India will be amongst the fastest-growing economies.

The changes are coming from following aspects

|

|

|

|

Big is getting bigger and strong

is getting stronger.

Trend started post demonitisation, then GST and now post Covid, the trend has accelerated significantly. In every sector the leaders are gaining market share:

- The top 6 banks over the last 3 years are dispersing 70% of the incremental credit.

- In cement, the top 5 companies have 90% of the incremental market share

- In steel, the top 5 companies again have 90% of the incremental business

- In housing finance companies, the 2 top companies have an incremental 90% market share

- In telecom, the 3 top companies have 100% incremental market share

|

Consolidations are seen in electrical cables, tiles, plywood, grocery retailing, and other home improvement companies. Market share is being taken away from the unorganised sector.

Further when you look at companies between 100 to 650 in size, about 200 of them are category leaders in the sector they operate in. Hence, it is not only the Mega large companies that are leaders. Over time, these companies will grow in size as they capture business from the unorganised sector.

|

|

Digitalization

This has brought the country as one and has brought immense opportunities and a platform for companies and the Government to distribute benefits, avail of benefits, etc. This is not going to change in a hurry. "Work from home" means work from anywhere. The economic growth will now not be limited to just a few cities but will be widespread. Every business has to develop a great digital ecosystem to grow their business. five years ago India ranked 122 on per capita data consumption. Now we are No. 1 in per capita data consumption along with the US and China. India will progress with 1 bn smart phones, 1 bn bank accounts and 1 bn aadhar cards - and any business which wants to scale up has no barriers of cost and geography. IPOs of about US $ 200 bn are lined up over the next few years of NEW AGE unicorns. Many of them will become large companies as they are leaders in their sector.

|

|

|

|

PLI / Atmanirbhar and the China plus strategy

March 2020 had US $74 bn FDI investment - 90% was through open route and 50% was for green field investments. There is a complete ecosystem that has started onshoring and the PLI has given it an accelerated push. The 13 sectors have been identified where we can become champions and this will revive the capex cycle. It will push backward integration, growth in exports, and this policy is linked to output. Capital Goods and Infra has done nothing over the last 10 years and this will give a push to that area.

|

|

Residential Real Estate

We are at the bottom of the cycle and should do well going forward. A large number of Real Estate companies do not make high Return on Equity - but the large number of ancillary companies will do well due to the real estate revival. The lower finance costs, high affordability levels, and the requirement of individuals working from home needing a large house, will benefit the revival of the real estate cycle.

|

|

|

|

Export Opportunities

Earlier, we used to be predominantly an IT exporting country. In the last 10 years we have seen Pharma becoming a major export industry. More recently we have seen tiles, and engineering goods grow their exports. In the next 10 years, many new sectors will also push exports.

|

|

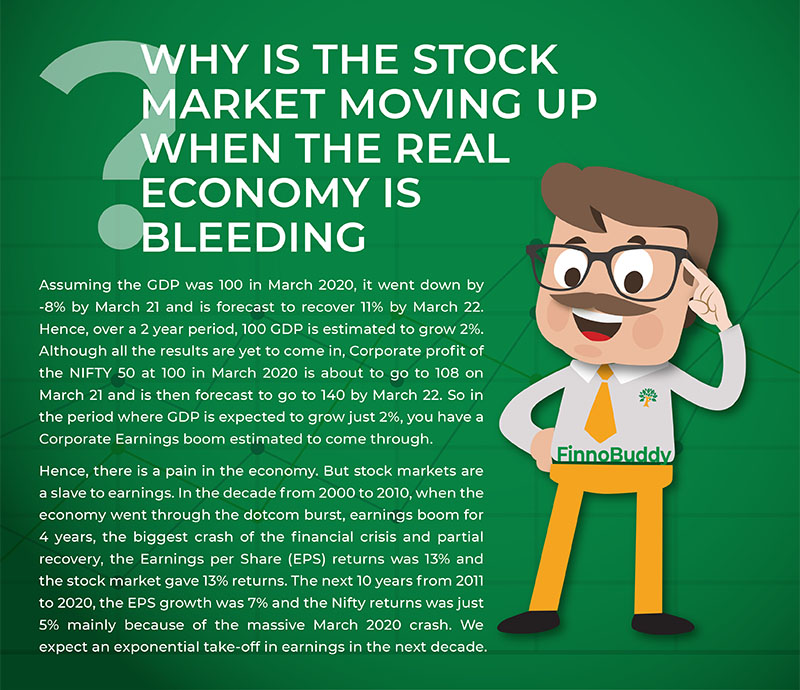

EQUITY

The equity market is definitely overvalued - most probably due to the flood of liquidity in the global economy and also in India. As the earnings growth has been low for the last 10 years, and if the earnings start picking up as they have been in December and March quarters, the valuations will become more reasonable.

Corporate earnings as a percentage of GDP - after hitting a low of 1.8% has currently hit a 4 year high of 2.6%. Although, the earning recovery may be slowed down by the partial lockdown with the 2nd Covid wave, this is likely to fall in the next quarter. However, the next decade is likely to be good for Emerging Markets and India. If in 5 years the corporate earnings as a percentage of GDP goes back to the long-term average of 4%, we are looking at about 18% returns. In the last growth cycle, Corporate earnings grew to 7% of GDP.

The major risk is the earnings growth gets derailed. Alternatively, if inflation grows and interest rates rise that too would slow growth.

|

|

|

|

DEBT

The 2nd Covid wave is a threat to growth and hence liquidity and low-interest rates are likely to remain accommodative. Returns in debt cannot be expected to be more than 5-6% over the next few years, especially, with the risk of rising inflation and hence rising interest rates.

Hence, we are looking at more innovative products like Liquiloans, although this is limited to Rs 10 lakhs per PAN holder.

As a part of your debt allocation, if you are looking at a 3 year term, and as we are bullish in equity over the next 3 years, you can look at conservative hybrid funds where the equity allocation is limited to 25% - and a few funds go even lower. The 3 year rolling returns are on an average 9-10% returns and could be a good option as a part of your long term debt allocation.

|

|

GOLD

Gold gained in May and touched a 4 month high, due to a weaker US dollar and rising price pressure. Gold is a hedge against inflation. Mass vaccinations will result in a strong economic recovery. However, Central Banks will keep interest rates low for longer than expected. Result is likely to be an inflation which is positive for gold. Further a weaker dollar too is positive for gold. China too, has re-opened imports of Gold. It did pass US $ 1900, and if it passes US$ 1920, it could breakout to US$ 2000 in the near term.

|

|

|

|

ACTION PLAN

- Invest in equity at all dips. The next 5 years look very positive for India.

- For longer term debt allocation, look at conservative hybrid funds.

- Hold on to your Gold investment.

|

|

|

| AKURDI |

WAKAD |

WANOWRIE |

MAGARPATTA |

B-20, Jai Ganesh

Vision, Akurdi,

Pune-411 035. |

No-1, Nisarg DeepApartment,

Kaspate Vasti Wakad,

Pune-411 057. |

No. 26, Shraddha Regency,

'A' Opp Kedari Garden, Wanorie, Pune-411 040. |

No. 14, 4th Floor, Destination Centre, Magarpatta City, Hadapsar, Pune-411 013. |

|

|

|

| Disclosure |

We are not registered as investment advisers and do not provide any investment advice. The information contained herein is for informational purposes only and does not constitute investment advice. We do not make any warranty (express or implied) as to information in this written material and do not assume any responsibility for, and shall not be liable for any losses or damages of any kind, resulting from investment in any investment product made on the basis of any information provided in this newsletter. Further, the information given herein is as of the date and time of this document/report/newsletter and there can be no assurance that future results or events will be consistent with this information.

Furthermore, certain data and other information may be obtained from a third- party feed, and we are not responsible for verifying the accuracy of the same. While we have taken due care and caution in the compilation of the data and the contents herein, no representation is made as to the reasonableness of the assumptions made within or accuracy or completeness of any data on past- performance of schemes or historical analysis and any other analysis of any investment products. We specifically state that we cannot be held liable for any damages (monetary, legal or otherwise) caused by any error, omission, interruption, deletion, defect, failure and that, we have no financial liability whatsoever to any user on account of the use of the information provided in this newsletter

|

|

|

|