|

- Extremely high debt to GDP, similar to what it was in the 1940s.

- Excessive market valuations at par with the 1929 and 2000 bubbles.

- A resource-driven inflationary crisis comparable to the 1940s.

- High valuations have started correcting. In the Nasdaq, there are more companies at a 52 week low that there have been in 30 years.

- Surge in energy prices suggests a high probability of a US recession.

|

|

|

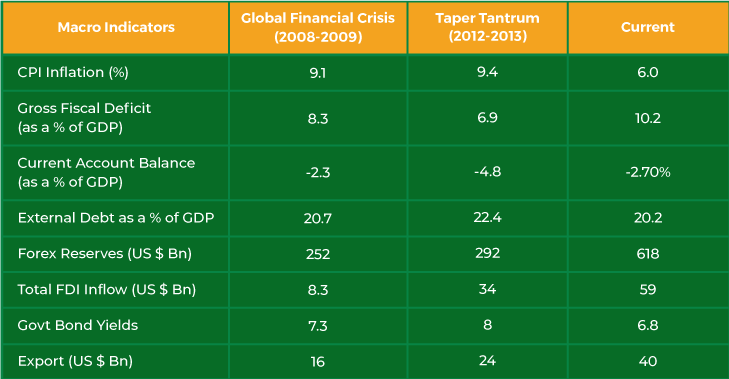

India's Macro Indicators position is much better now that during Global Financial Crisis (2008) and Taper Tantrum (2012-13)

|

|

India is at the beginning of the business cycle recovery. This is reflected in the fact that India's Capacity

Utilisation is below its long term average, whereas developed markets like the US are well above the

long term average. India's capex is rising and is expected to increase further.

|

|

India's Economy is relatively less affected by Geo Politics.

- India's policy environment is much more certain and strong - aimed at driving growth, like the PLI scheme.

- Oil consumption relative to GDP is low and has been on a steady decline since 2014.

- India's real policy rates relative to global economies remains high (better to tackle inflation arising from high oil prices).

- Rising share of FDI to FPI (FDIs own ca ontrolling stake in a company by investing in its physical assets while FPIs invest only in Financial Assets) in external balances makes the economy less sensitive to short term withdrawals.

- INR has been relatively more stable compared to previous oil shocks.

|

|

|

|

EQUITY MARKETS

-

There has been a Central Bank bull market from 2008 right up to 2021, with a small hiccup at the time of the Taper Tantrum. Even in April 2021, the Federal Reserve announced that inflation was transitory and interest rates would not rise until 2023. By December 2021, the Federal Reserve changed and said that Inflation was more sticky and interest rates would be rising soon. Mainly supply-side inflation is rising all over the world including Japan, which has been experiencing negative to low inflation for decades.

-

Foreign investments have withdrawn Rs 1.48 lakh crore funds between October 2021 and March 2022. It is the strength of the retail investor which has been buying at every dip. Further, the monthly SIP collections is at over Rs. 12000 crores. As long as this continues, there will not be any large fall in the equity market, but if the sentiment does change we could see a deeper correction.

-

There is no real worry about corporate earnings yet. Commodity companies are doing well and so is banking. Other sectors may see some inflation pressures, but once the supply chain gets normalized - India is well placed with the revival of the Capex cycle.

|

|

DEBT MARKET

In the last RBI policy, the Repo rate was kept unchanged at 4%, whereas the Reverse Repo rate was raised by 40 bps to 3.75%. The policy was under the background of:

The Governor stated that the priority is now controlling inflation, before growth. Without raising interest rates, the 10 year G Sec yield has gone up from 6.8% to about 7.2%. We can expect further rate hikes going forward.

|

|

|

|

GOLD

Reasons why we need to hold gold:

-

Geo-political risk

-

Sticky inflation, with negative yields in the US.

-

Volatile stocks

|

|

ACTION TO BE TAKEN

-

Invest through at least an 18-month SIP / STP as the market is likely to continue to be volatile.

-

At least 10-20 % of your equity exposure should be global fund.

-

Asset allocation of all asset classes is essential, including gold.

One can be overweight on gold.

|

|

|

|

| AKURDI |

WAKAD |

WANOWRIE |

MAGARPATTA |

B-20, Jai Ganesh Vision, Akurdi,

Pune-411 035. |

No-1, Nisarg Deep Apartment,

Kaspate Vasti Wakad,

Pune-411 057. |

No. 26, Shraddha Regency, ’A’ Opp Kedari Garden, WANOWRIE,

Pune-411 040. |

No. 14, 4th Floor, Destination Centre, Magarpatta City, Hadapsar,

Pune-411 013. |

|

|

|